Australia’s answer to “open banking” – the Consumer Data Right, or CDR – is picking up steam. We’ve reached a tipping point where more consumers are sharing data from more banks with more financial services across more use cases, and with those growing numbers we can now reliably measure and contrast performance from bank to bank.

Typically, performance based metrics are challenging to determine because the information needed is just not available. The limited performance measure that is public is the number of banks sharing data via Open Banking and their ‘uptime’, which as of January 2023 sat at over 99%, and only refers to the connection success rate.

Additionally, there is no way to easily compare how financial institutions (the data holders) are stacking up; who is leading the way and who is underperforming?

And let’s not forget the heart of the CDR – the consumer. As a business, I know you want to know how many consumers are using CDR and, most importantly, the conversion rate.

The good news is:

- Firstly, Basiq is in a unique position to generate these insights into Open Banking. Our depth of knowledge and experience using web connectors (also known as ‘screen scraping’) means we are able to directly compare the performance of both data access methods. Via Basiq’s platform, we also have the highest number of business customers accessing Open Banking, across the widest range of active use cases in market, which enables us to measure and monitor these performance metrics that matter.

- Secondly, you have me, a customer advocate and certifiable data nerd at Australia’s leading open banking platform, to crunch the numbers, tell the stories and push for more accountability.

Today I’m going to look at consumer experience (CX) and conversion: why it matters, how we measure it, and how the data holders stack up. In future posts I’ll pick out other stories but I’ll track and update the CX leaderboard each month.

But first, we need to talk about …

“The state of Open Banking”

I’ve got that in quotes because I’ve seen the phrase so often the words have lost all meaning! It’s a hot topic though, with some voices in the media saying that CDR is not ready to support all use cases (actually I agree – but this argument misses the point. Did Google support search, maps, email, docs, translate, meetings and forms all on day one?)

CDR is young and there are gaps but it is already delivering value for our partners in investing, lending, payments, early wage access, the green economy and personal finance management to name a few.

Screen scraping (“scraping”) is the precursor to Open Banking. It’s also the data access method Basiq was founded on in 2017 and has used extensively since. For our customers who have transitioned to open banking (with the same use case, requesting access to the same banks and using the same user experience) we are seeing a 10% increase in the number of customers converting and sharing their data through CDR compared to scraping.

Use cases which got value from scraping are getting value from CDR today.

The quality of data from CDR is on a par with that from scraping: in some cases it’s great and in others it’s not what you would hope. Under scraping we developed a resilience to gaps in banking data quality, and we’re using those same smarts to help our customers under CDR.

To get the most from CDR you’ll need to make some tweaks to your UX, we can help you with that; there are a few banks who are more stable with scraping than CDR, we can guide you on that too. But this blanket argument that CDR is not ready does not jibe with what we’re seeing.

Consumer experience and conversion

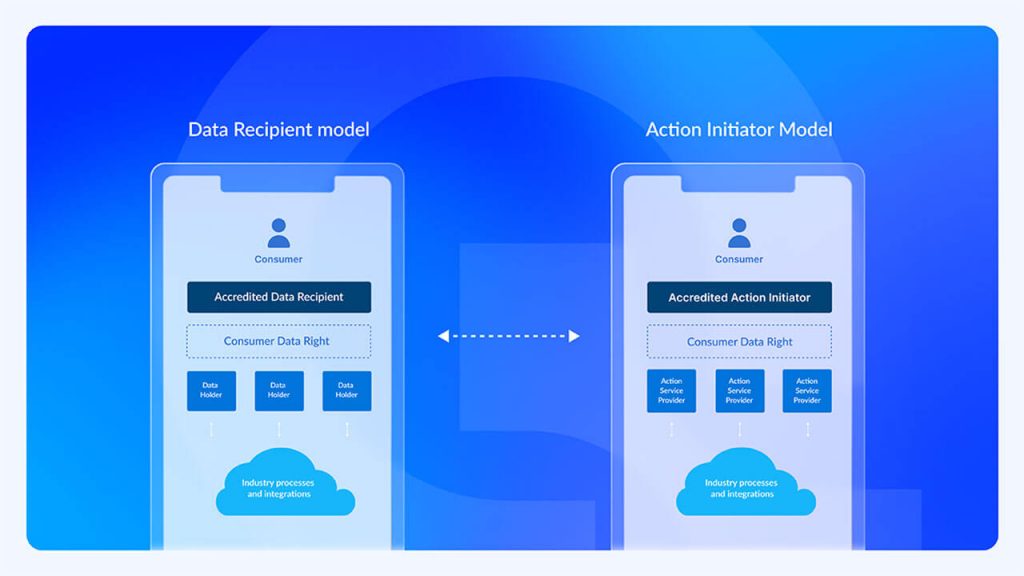

Under CDR, when a consumer wants to share their data they are redirected from the recipient (e.g., a financial app or lending platform) to the data holder’s portal via Basiq platform (i.e., the consumer’s bank or financial institution), where they authenticate securely with the data holder, acknowledge the recipient’s request for data, and select and share their accounts. At the end the consumer is redirected back to the recipient. By design, the data holder’s portal is a black box to the recipient and the experience is inconsistent because each data holder handles this process differently.

That’s great for security and privacy and ensuring an informed and free consent to share data – but it’s a huge challenge for businesses in the digital age to “throw a user over the fence” and blindly hope they’ll come back. If the user doesn’t return, often it’s impossible to get the reason why.

For our customer experience benchmarks at Basiq, we have our customers top of mind and measure data holders on the below criteria:

- Consumer conversion vs drop-off in the data holder’s portal ✅

- Consumer time spent in the data holder’s portal ⏱

- Consistency and quality of data returned ℹ️

- Speed to return data ??♂️

Data Holder CX Leaderboard | January 2023

Now, let’s get to the exciting part… my commitment to you.

Each month I’m going to rank the performance of the top 10 Data Holders, plus any of the big 4 who fall outside the top 10.

I’ll look at how the banks performed across all four metrics but with a weighting on conversion – because without consumers sharing their data there’s not much of a Consumer Data Right.

Then I’ll wrap that all up and just tell you how they ranked so that you don’t have to sweat the details.

Results are in for January 2023

If you had Bananacoast CCU on your bingo card, you’re a winner! Kudos to the BCCU team for a great result. (Disclaimer: we have no relationship with BCCU, I just know good performance when I see it.)

Our top 10 performing data holders for January

")

")

- Up Bank are setting the gold standard for CDR CX: they consistently have the highest conversion and fastest user journey, and are on par with other top performers for quality and speed

- ANZ are best of the big 4, taking over from NAB last month

What does this mean for the state of Open Banking?

We saw conversion across all data holders lift by 8% in January as consumers become more confident with the CDR experience and data holders refine their user experience.

Most banks are lifting their game on all key CX metrics, but a few are continuing to struggle.

We recommend a pragmatic approach to switching from scraping to Open Banking: let us know your needs and appetite and we will suggest high value banks to add now, with a staged plan to add support for more banks as they mature.

In other news

Qudos Bank started blocking screen scraping in December. Basiq has decommissioned the Qudos web connector but the CDR connector is working well.

Basiq customers on v3 of the API who have access to CDR are able to switch their Qudos users dynamically from scraping. Other customers, if Qudos is important to you or your users, please reach out to us to see if CDR is a good fit for you.

If you’re interested in CDR and consumer experience

… please reach out! I would love to hear your thoughts about this – we are all learning. Please also send any ideas or questions for next month’s post to me at alex@basiq.io.

You might also be interested in the articles and resources below:

- How Open Banking is benefiting businesses

- How access to customer banking data is changing

- The difference between screen scraping and Open Banking

- Why now is the time to make the move to Open Banking

- Choosing an Open Banking provider

Article Sources

Basiq mandates its writers to leverage primary sources such as internal data, industry research, white papers, and government data for their content. They also consult with industry professionals for added insights. Rigorous research, review, and fact-checking processes are employed to uphold accuracy and ethical standards, while valuing reader engagement and adopting inclusive language. Continuous updates are made to reflect current financial technology trends. You can delve into the principles we adhere to for ensuring reliable, actionable content in our editorial policy.